Estimating the locations, volumes and values of undiscovered oil and gas resources is a complex task. The petroleum geology and exploration processes must be fully understood, as well as the fiscal environments of future exploration and production activities.

What does the last 20 years of global exploration tell us? The industry makes its money in and around proven charge areas. They do approximately correspond to areas with existing infrastructure. As such, they correspond to the main current focus areas for investments, which offer shorter development times than the more remote and riskier areas.

Although the energy transition is underway, the world still needs oil and gas. The recent turmoil in Europe highlights the need for energy security and an over-reliance on foreign imports. Ongoing commodity price challenges have forced the global energy industry to scale back on exploration. There is not a quick fix for this situation. The time period from discovery to development is long, ranging from five to 20 years, and production could span from 10-50 years.

Oil and gas resources will remain a critical piece of the world’s energy supply, even as we transition to decarbonization. Given the long time period associated with discovering and developing oil and gas resources, a continued focus on infrastructure-led exploration is required.

Limitations of existing undiscovered resource estimates

Publicly available estimates of the world’s remaining oil and gas potential have been made by various organizations. The most quoted and comprehensive of these is the USGS World Petroleum Resources project, which is an active project focused on the assessment of oil and gas resources across the world. This impressive project defines future resources as “technically recoverable” volumes, meaning that the oil and gas can be produced using currently available technology and industry practices. However, this estimate does not consider any economic or accessibility constraints. This is a major limitation, as economic factors, geopolitical risk, and access to infrastructure impact the commerciality of technically recoverable resources. Resources that are below a certain volume or located in remote areas may never be economically viable at any commodity price.

New solution for estimating remaining conventional oil and gas resources

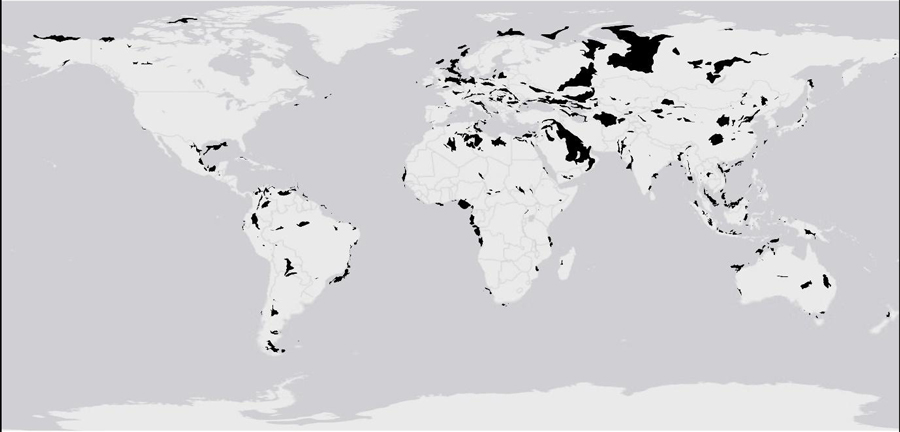

IHS Markit, now a part of S&P Global, joined forces with GIS-pax to develop a global evaluation of conventional resources (excluding the Lower 48 and shallow water Gulf of Mexico) specifically designed to forecast both geological and related commercial volumes. The solution, called Portfolio Opportunity Ranker, provides stochastic results in proper spatial context. Values can be aggregated at multiple levels of granularity, including basins, countries, and large blocks. Equity-level evaluations can also be compiled to help value individual company portfolios. The released estimates presented in this article include future predicted discoveries for areas with proven charge, as defined from IHS Markit spatial oil and gas data (Figure 1). The evaluation incorporates the risk and volume assessment of more than 21,000 identified prospects, as well as a systematic estimate of the remaining but currently unidentified prospects (yet-to-find). The methodology for the unidentified prospectivity is based on a proprietary methodology that uses machine learning of the geology and exploration history to predict future prospect counts and volumes.

Figure 1. The areas of proven charge, as defined by IHS Markit discovery data (fields, reservoirs and well data), incorporated into the yet-to-find assessment. Note that onshore North America (Lower 48) and shallow water GOM is excluded.

Economic and commercial volume calculations

It is important to distinguish between geologic, commercial and economic volumes when estimating global undiscovered oil and gas resources. Not every oil and gas resource in existence is economically or commercially viable, due to a variety of factors.

The geological volume of a resource is the predicted volume of hydrocarbons that will be found in a defined area using the currently available technology and industry practices. These estimates are generally considered to be academic/theoretical estimates, as they do not consider any economic or accessibility constraints. The USGS estimates of technically recoverable resources are comparable to geological volumes.

The commercial volume of a resource is the geological volume of hydrocarbons in an area above a certain volumetric threshold. Commercial volume is estimated for oil and gas fields separately in areas of perceived equal value (i.e., same bathymetric band or similar distance to infrastructure) using detailed evaluations of undeveloped assets where an estimate is made of the minimum volume required to be NPV=0. This volume is typically expressed as an oil-equivalent threshold volume for oil fields and gas fields accordingly.

Economic volume of a resource is the minimum field size that will earn money, determined for a variety of commodity prices. Calibration data are used to predict a range of value metrics for different oil prices for each polygon above the low/base/high value estimates. These data can be used to calculate the risked NPVs (Expected Monetary Values).

Robust estimates of global yet-to-find with Portfolio Opportunity Ranker

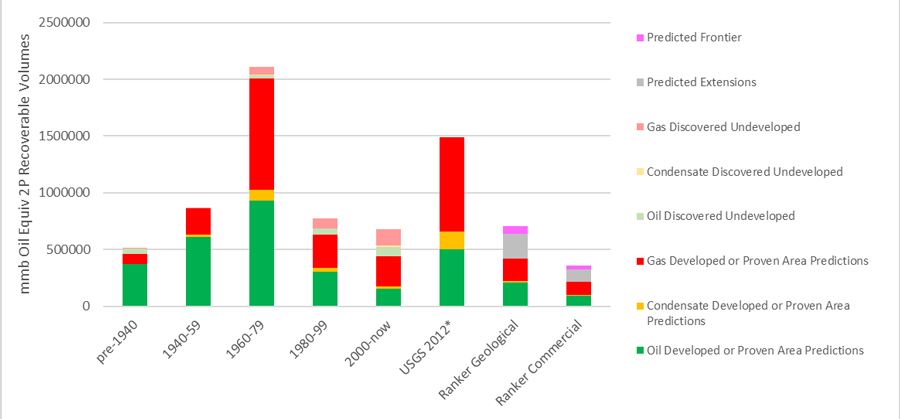

Figure 2 shows a summary of historical discovered 2P recoverable hydrocarbon volumes by commodity and current development status for 20-year time intervals over Portfolio Opportunity Ranker’s study area (shown in Figure 1). This figure also shows a comparison of the corrected USGS volumetric estimate (published in 2012) and those from Portfolio Opportunity Ranker.

The USGS technically recoverable volumes are two times the Portfolio Opportunity Ranker geological estimates and four times what Portfolio Opportunity Ranker estimates for future commercial volumes. Portfolio Opportunity Ranker’s geological estimates do not consider commercial limits, while the commercial volume estimates are limited by commercial volumetric cut-offs determined from a variety of factors including fiscal terms, distance to pipeline and bathymetry/distance to coastline/elevation as applied separately to oil and gas field developments.

The IHS Markit Vantage valuation dataset is used to calibrate commercial cut-offs commensurate with the current fiscal regimes active in all countries. The current Portfolio Opportunity Ranker estimate shown by commodity type in Figure 2 is only for the proven charge areas shown in Figure 1. Based on a lookback analysis to 2000, we believe that ~60% of the future total volumes will be in the proven charge areas, 30% will be in extensions of existing proven charge areas and the remaining 10% will be in future frontier charge cells that are yet to be discovered.

Figure 2. Historical and future predictions of conventional hydrocarbon resources in the study area. Note the USGS 2012 estimate has had subsequent post 2012 discovered volumes removed from the estimate.

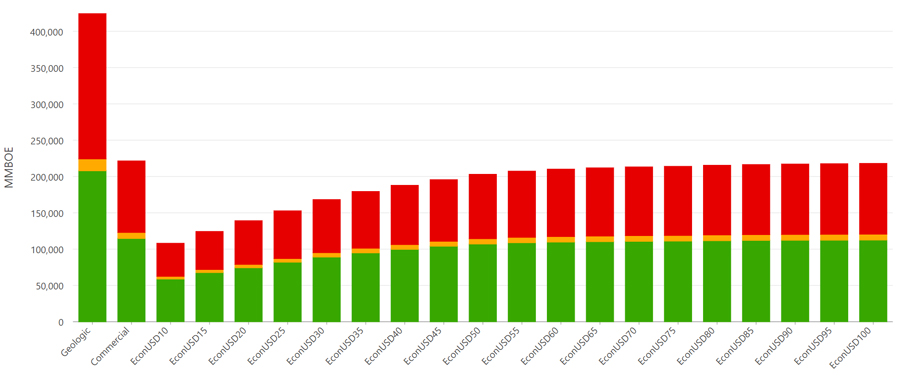

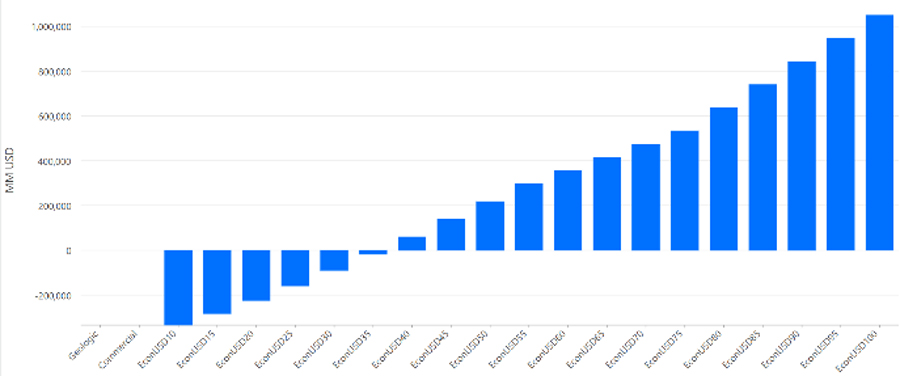

Based on the Portfolio Opportunity Ranker evaluation, we can estimate the future volumes of oil and gas with no economic filters, with economic filters and for 19 different oil prices as shown in Figure 3. For these evaluations we can also estimate the total value of these oil price cases, as shown in Figure 4.

These data demonstrate that the tangible yet-to-find for conventional oil and gas is strongly dependent on commodity price. The potential profits from future exploration range from more than US$1000 trillion at USD100/barrel to US$0 at USD35/barrel. This suggests that the effective yet-to-find for the industry is roughly zero at the lower oil price ranges. Exploration in these low oil price cases will still deliver a few large discoveries and economic volumes (Figure 3) but overall, the business will be value destructive (Figure 4).

Figure 3. The future estimated volumes of recoverable oil, gas, and condensate volumes for total geological and commercial estimates, as well as 19 economic cases for areas of proven charge excluding L48 and shallow-water GOM.

Figure 4. The estimated value in MMUSD of future recoverable oil, gas, and condensate volumes for 19 economic cases for areas of proven charge excluding onshore L48 and shallow-water GOM.

These yet-to-find estimates do not include play extensions or new future petroleum province volume estimates. They do, however, approximately correspond to areas with existing infrastructure. As such, they correspond to the primary current focus areas for investment, which offer shorter development times than the more remote and risky areas. We do not make predictions for future frontier proven charge cells beyond the percentage estimate however we do spatially limit where they may be and provide an analogue library for these opportunities.

Fuel for the energy transition

Our methodology suggests that only ~13% of the conventional global resource base remains to be discovered, which will deliver an additional ~7% to global commercial volumes (Figure 3). The estimated remaining commercial volumes highlight a previously unrecognized demand-driven requirement for the energy transition, given that the estimated future commercial volumes presented here will likely deliver less than five years of global energy supply at current consumption rates.

Transportation is a key element of the energy transition. Today, cars and light vehicles consume around 35% of the 100 million barrels of oil produced daily. Although vehicle electrification is underway, it will take years or even decades to fully electrify the global transportation fleet. Also, the power grid is at capacity in many countries, straining the ability to power electric vehicles. Considering that it takes more than five years to discover and develop an oilfield, investments into new upstream projects should remain a key focus throughout the energy transition.

Learn more about POR

About Portfolio Opportunity Ranker

This new product is available through a regional or global subscription. It is designed to assist stakeholders in making better decisions about future investments. Updates will be delivered every six months capturing exploration activity, license and fiscal changes. Portfolio Opportunity Ranker is delivered in a GIS database platform with software that enables customers to modify all key inputs and generate their own internal evaluations incorporating their own prospects and portfolio assumptions. The workflow is simple and industry standard, it is editable and auditable. It is not a black box. The product is also delivered with a global evaluation done by an experienced exploration team with a cumulative 250 years of international exploration experience. Additionally, a consulting service is offered to governments and other commercial organizations to assist them with extracting the most value from their subscription.

About S&P Global Commodity Insights

At S&P Global Commodity Insights, our complete view of global energy and commodities markets enables our customers to make decisions with conviction and create long-term, sustainable value.

For more than 100 years, we've been a trusted connector that brings together thought leaders, market participants, governments, and regulators to co-create solutions that lead to progress. Vital to navigating Energy Transition, S&P Global Commodity Insights' coverage includes oil and gas, power, chemicals, metals, agriculture, and shipping.

About GIS-pax

GIS-pax is a private company based in Australia that has built and specializes in play analysis software for both the conventional and unconventional global oil and gas E&P industry. Our software was created from the ground up incorporating 60+ years of global geological exploration expertise and GIS E&P company experience.

Our products have become the gold standard tools for Play Analysis in the upstream oil and gas industry today. Our client list is comprised of 30+ international E&P companies from small independents to global supermajors that are actively exploring almost every basin on the planet